Author(s):

Ramin Wright

Nov 10, 2016

As part of Osler’s focus on cross-border transactional activity, we analyze deal flow between Canada and the U.S. in order to update our readers on macro trends in deal flow between the two countries. As summarized below, our review of cross-border transactional activity through September 2016 shows continued growth in the strong ties held between the Canadian and U.S. financial markets, with Q3 2016 showing a 5-year high in the value of outbound M&A activity from Canada to the U.S.

Background

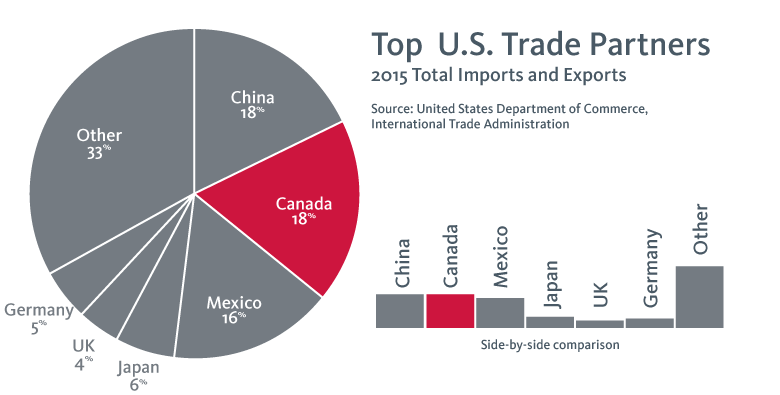

The economies of the United States and Canada are among the most highly connected in the world, with bilateral trade between the countries exceeding CDN $2.4 billion per day. Cross-border trade among these countries is central to the vital economic interests of both countries. For example, Canada is the second largest international trade partner of the United States (behind only China, a country with a population 38 times larger than Canada), accounting for approximately one fifth of total U.S. international trade.

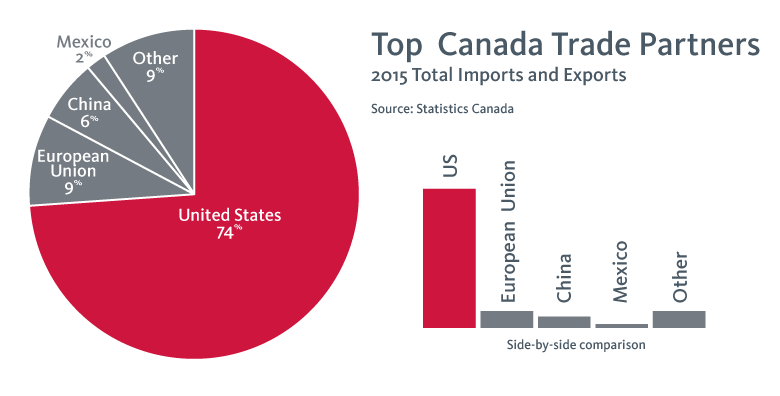

Even more dramatically, approximately 74% of Canada’s total imports and exports by value is attributable to trade with the United States. Given this degree of economic interconnection, the free and efficient flow of capital, goods and services between Canada and the U.S. is fundamental to the strong and stable functioning of Canada’s current and future economy. On a more micro-economic level, the ability of Canadian businesses to strategically access U.S. markets for capital, customers or M&A opportunities is often critical to their growth opportunities.

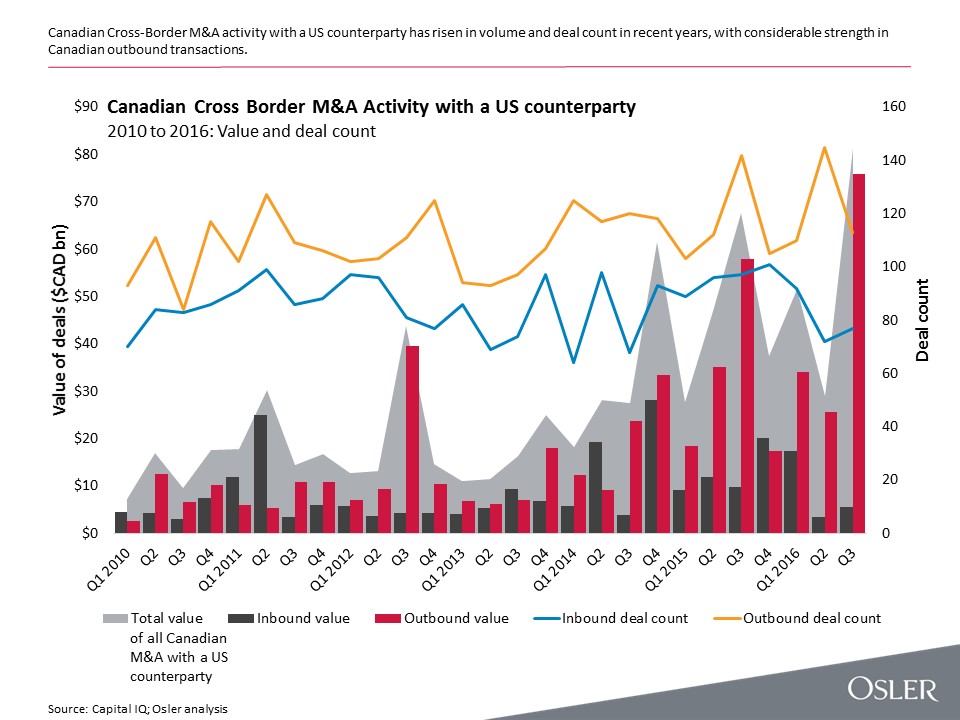

In the discussion below, we provide a brief snapshot summary of how this vital cross-border transactional marketplace performed in Q3 2016. In this discussion, “inbound” transactions refer to those transactions where the dominant geography of the target company is Canada and the dominant geography of the bidder is the United States, while “outbound” transactions are those with these qualities reversed.

Aggregate deal flow across the Canada-U.S. border

It is evident from recent growth in M&A activity across the Canada-U.S. border that investment and deal-flow between the neighbouring countries remains strong and that outbound deal value continues to trend upward. Aggregate Canada-U.S. cross-border M&A in the last twelve months slipped slightly to $194.3bn, down 4.8% from the twelve months prior. Overall, recent M&A activity between Canada and the United States is weighted towards outbound investment from Canada into the United States - between 2010 and 2016 YTD, 67.6% of Canada-U.S. cross border activity involved the acquisition of a U.S. target by a Canadian buyer.

Size of Canada-U.S. cross-border deals

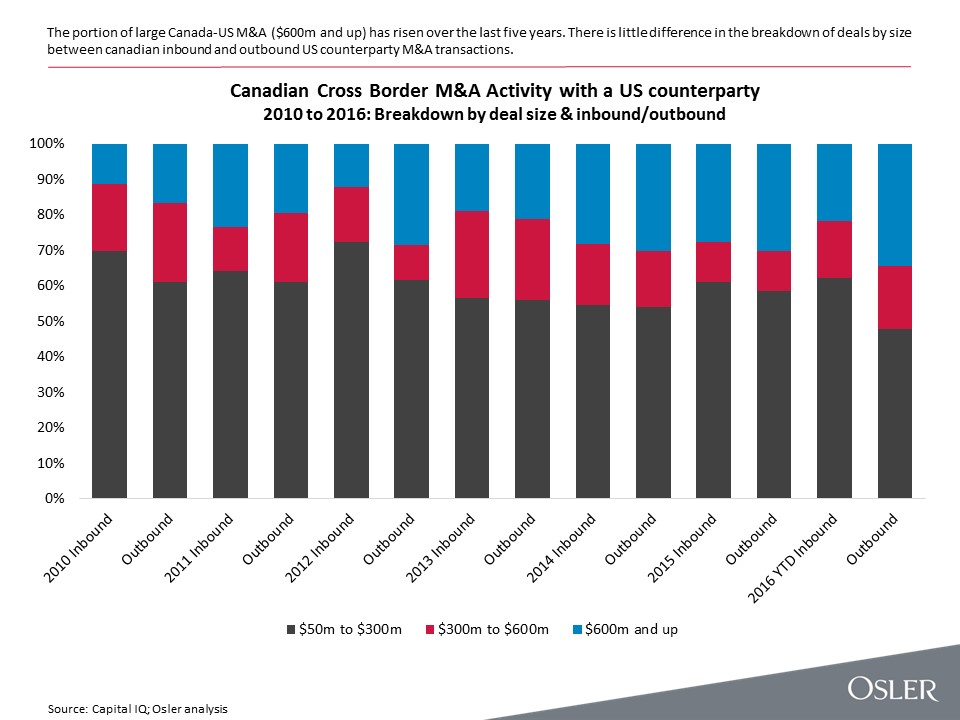

Canada-U.S. cross-border M&A shows a fairly consistent weighting towards mid-size deals, with an average 60% of value being attributable to deals sized between $50m and $300m CAD over the period reviewed, a trend that is (on both an inbound and outbound basis) relatively unchanged since 2010. This time period shows no significant difference in the most common deal sizes when comparing acquisitions by a US and Canadian buyer of a cross-border target. Overall, deals sized above $600m CAD account for 24% of the Canada-U.S. cross-border market since 2010.

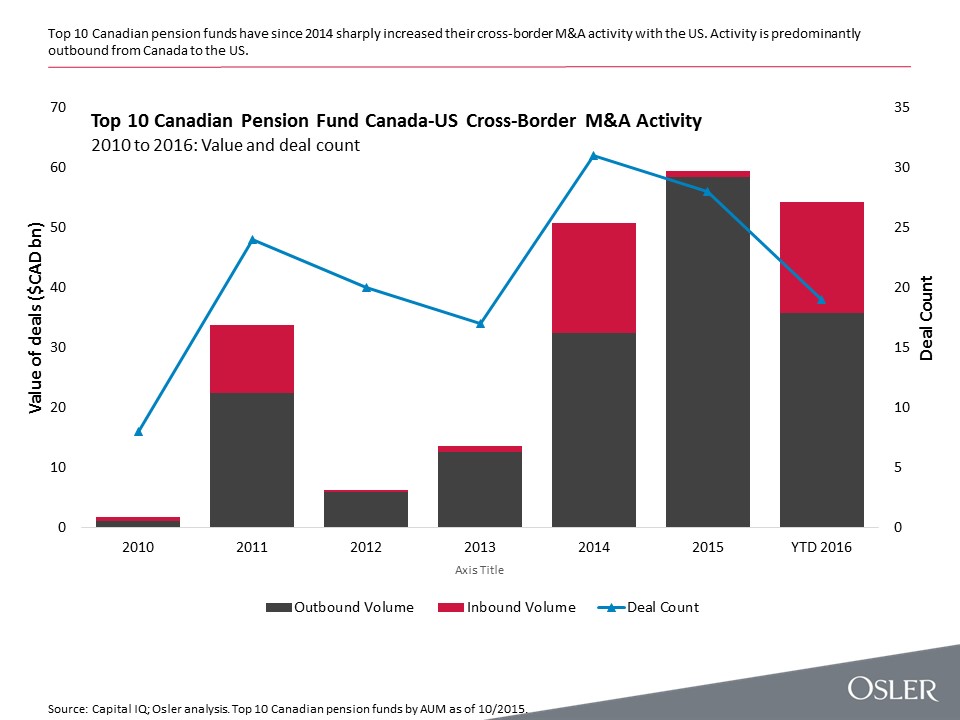

Canadian pension fund deal flow across the Canada-U.S. border

Large Canadian pension funds helped fuel the growth trend in Canada-U.S. cross-border M&A, with the aggregate value of their cross-border M&A activity between the two countries growing at a 79% CAGR since 2012 projected to the end of 2016. This growth occurred during a period of a declining Canadian dollar, showing the appetite for Canadian pension fund investment in the United States remains strong despite currency-based increases in effective asset prices.