Author(s):

Justin Dharamdial, Matthew T. Oliver

Apr 4, 2014

On March 20, 2014, the Canadian Securities Administrators (CSA) published a notice (the CSA Notice) announcing the release for comment of two proposed equity crowdfunding prospectus exemptions. Some provincial securities administrators released for comment the proposed Multilateral Instrument 45-108 respecting Crowdfunding (the Crowdfunding Exemption) with accompanying policy statement; others released for comment a proposed Blanket Order respecting Start-Up Crowdfunding Prospectus and Registration Exemption (the Start-Up Exemption).

Equity crowdfunding enthusiasts in Canada have been awaiting regulatory action ever since the Ontario Securities Commission (OSC) released a staff consultation paper (the Consultation Paper) in December 2012, which contemplated a prospectus exemption for equity crowdfunding. We followed the public commentary with respect to the Consultation Paper and outlined the more salient stakeholder responses in a previous Osler Update, available here.

In this Osler Update, we outline the jurisdictional landscape proposed in the CSA Notice, as well as provide a brief comparison of substantive regulations proposed in the two prospectus exemptions.

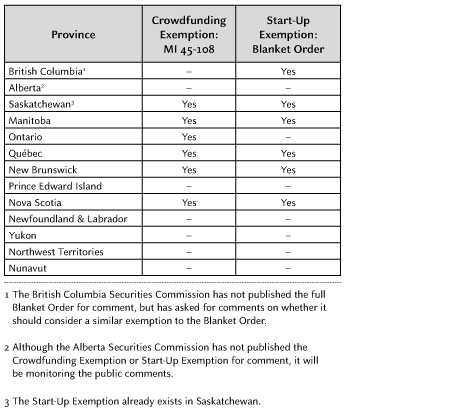

Jurisdictional Landscape

This chart shows the jurisdictional landscape proposed by the CSA Notice:

If these proposals are adopted without changes, there would be four types of provincial crowdfunding jurisdictions in Canada: (1) Crowdfunding Exemption only; (2) Start-Up Exemption only; (3) both Crowdfunding Exemption and Start-up Exemption; and (4) neither Crowdfunding Exemption nor Start-up Exemption.

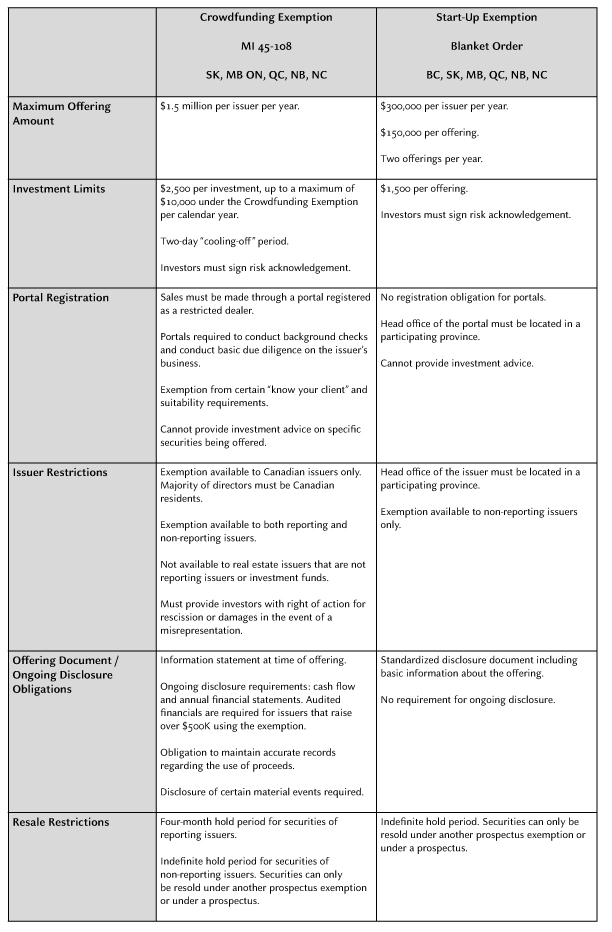

Comparison of the Crowdfunding Exemption and the Start-Up Exemption

The jurisdictions that introduced both the Crowdfunding Exemption and the Start-Up Exemption believe that the proposals complement each other, as each proposal focuses on capital raising for companies at different stages of growth and development. The Start-Up Exemption contemplates a less onerous regime for issuers: there are no dealer registration obligations for crowdfunding portals and no requirement for issuers to provide ongoing disclosure. But as a result, an issuer relying on the Start-Up Exemption can raise only $300,000 per year. Under the Crowdfunding Exemption, an issuer would be able to raise up to $1.5 million per year, but undertakes a more onerous amount of regulation, including ongoing disclosure obligations.

This chart more fully compares the salient features of the Crowdfunding Exemption and the Start-Up Exemption:

Conclusion

The CSA has expressed the view that equity crowdfunding can be a viable method for start-ups and small and medium enterprises to raise capital. The two proposed crowdfunding prospectus exemptions have attempted to strike different balances between investor protection and access to capital markets.

Companies interested in sourcing capital through one of the crowdfunding exemptions should be aware that, depending on the jurisdictions in which they or their investors are based, different regulatory regimes may apply.

The bifurcated regulatory framework proposed by the CSA Notice may be instructive of the varying views of its member provincial securities administrators. We should consider whether the OSC, in not proposing the Start-Up Exemption alongside the Crowdfunding Exemption, may be signalling certain investor protection concerns with the Start-Up Exemption.

The comment period on the crowdfunding prospectus exemptions closes June 18, 2014. For more information about this topic, please feel free to contact Matthew Oliver or Justin Dharamdial.

Authored by Matthew Oliver, Justin Dharamdial