Authors

National Co-Chair, Toronto

Partner, Corporate, Toronto

Partner, Corporate, Toronto

While the declaration of the novel coronavirus (COVID-19) as a global pandemic in Q1 – and its subsequent impact – resulted in a sharp decrease in deal volumes in the first and second quarters of 2020, deal volumes rebounded strongly in Q4. This article provides an overview of those trends as well as some of the most notable Canadian legal developments in public M&A in 2020.

COVID-19 market and deal term impacts

COVID-19 had a profound impact on Canadian M&A volumes and deal terms in 2020. It also led to several high-profile deal terminations and renegotiations.

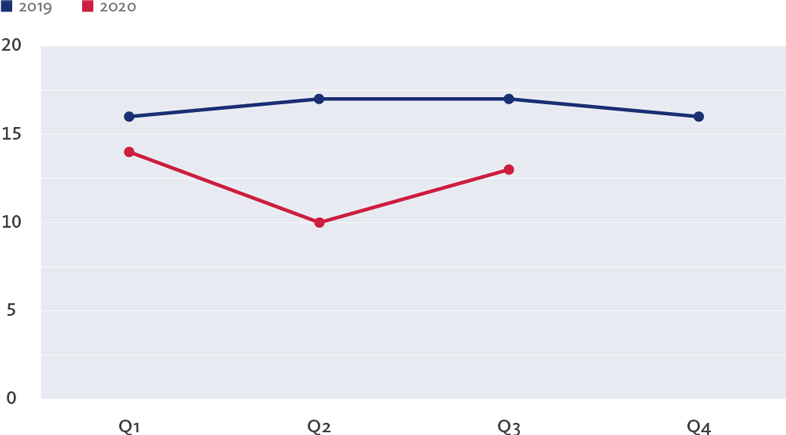

As of October 30, 2020, there were 40 announced acquisitions of Canadian public companies in 2020, as compared to 58 for the same period in 2019 according to Practical Law Canada. Deal volumes at the start of 2020 were slightly lower than in 2019. This was followed by a significant decline at the outset of the pandemic, with volumes recovering in the latter half of 2020, albeit not to 2019 levels.

FIGURE 1 NUMBER OF CANADIAN PUBLIC COMPANY ACQUISITIONS BY QUARTER

The COVID-19 pandemic also focused attention on the precise wording of material adverse effect (MAE) definitions and interim operating covenants.

An MAE clause is a standard provision in M&A agreements that generally allocates business-specific risks to the target and economic and market-based risks to the buyer. The provision states that, where an MAE occurs before closing, the buyer is not obligated to complete the transaction, either structured as a condition or as a termination event for the purchaser.

MAE definitions routinely contain exceptions for the benefit of the vendor, including for general economic and industry conditions, unless those conditions cause a “disproportionate impact” on the vendor. They often include additional exceptions for events such as war, terrorism and natural disasters, which (if included) are typically also subject to a “disproportionate impact” standard. Since April 1, 2020, our research indicates that approximately 87% of negotiated Canadian public company M&A deals have included a carve-out for pandemics, epidemics or similar outbreaks of illness, and approximately 65% of negotiated Canadian public target M&A deals now include an explicit reference to COVID-19 in the MAE carve-outs.

Interim operating covenants to which companies are subject between signing and closing now frequently feature COVID-19 exceptions, although the breadth of these exceptions and degree to which the target must consult with the buyer in order to avail themselves of the exception varies considerably. Since April 1, 2020, our research indicates that approximately 52% of Canadian public target M&A deals have carved out “COVID measures” or a variation thereof from the restrictions on the target’s business conduct covenants.

Although a substantial body of case law on MAEs has developed in the United States, there has been a dearth of Canadian case law on the topic until a December 2, 2020 decision of the Ontario Superior Court of Justice. In Fairstone Financial Holdings Inc. v. Duo Bank of Canada, a private transaction, the Court found that no MAE had occurred, nor had the ordinary course covenants been breached by actions taken by the vendor in response to the COVID-19 pandemic, awarding specific performance in favour of the vendor.

In Fairstone, the Court adopted a legal test for an MAE similar to the test that applies in Delaware, requiring an unknown event, a threat to overall earnings potential and durational significance. While each of those were established, the Court found no MAE as there was an exception for material adverse effects resulting from, among other things, emergencies.

In interpreting whether the ordinary course covenants had been breached, the Court found that the ordinary course covenant should be read in the context of the entire transaction. Given the emergency exclusion in the MAE clause, it would not be appropriate to use the more general ordinary course provision to effectively override the more specific MAE provision. The Court also found the target’s response to the pandemic was consistent with its practices in allowing the target to continue its day-to-day operations.

The Court’s decision in Fairstone stands in stark contrast to the November 30, 2020 decision of the Delaware Court of Chancery in AB Stable VIII LLC MAPS Hotels and Resorts One LLC, et al. In that case, the Delaware Court found that significant changes to the target’s business in response to the COVID-19 pandemic violated the target’s covenant to operate its business in the ordinary course consistent with past practices. The Court’s finding on this point was made despite the Court also having concluded that the pandemic did not constitute an MAE as it was excluded from the definition by an exception..

Three Canadian public M&A transactions that were announced pre-pandemic were terminated or renegotiated following the declaration of COVID-19 as a global pandemic; one of these remains the subject of pending litigation. We are aware of other private M&A transactions announced prior to the pandemic that have been the subject of renegotiations, as well as threatened or pending litigation.

| Buyer/Seller | Announcement Date / Termination or Renegotiation Date | Status | Cause for Litigation or Renegotiation |

|---|---|---|---|

| Air Canada / Transat AT | June 27, 2019 / October 9, 2020 | Parties renegotiated transaction, reducing consideration from $18/share to $5/share | Transat required consent to put in place a short-term debt facility/ possibility of not obtaining regulatory approvals prior to outside date |

| Cineworld / Cineplex | December 15, 2019 / June 12, 2020 | Cineplex has commenced an action in the Ontario Superior Court of Justice seeking damages for loss of bargain | MAE / failure to operate in ordinary course |

| CanCap Management / Rifco | February 2, 2020 / March 30, 2020 | Settled for $1.5 million (5.9% of transaction value, and 50% more than negotiated termination fee) | MAE |

New guidance on special committees and going private transactions

The Ontario Securities Commission’s (OSC) reasons for its decision in Re The Catalyst Capital Group Inc. has important disclosure and procedural implications for material conflict of interest transactions. Although the OSC did not cease trade the privatization proposal by a group of shareholders led by management of Hudson’s Bay Company (HBC), it ordered remedial disclosure to address what it determined were a number of disclosure deficiencies and required the mailing of a blacklined circular to HBC shareholders. The OSC was also critical of the fact that certain business judgments were made by HBC’s lead director prior to the formation of a special committee of independent directors.

The decision reinforces the importance of establishing a special committee and the engagement of independent legal and financial advisors early in the process of considering a material conflict of interest transaction. It further emphasizes the need for detailed disclosure of key judgments made in the course of board deliberations and the process for reviewing and approving the transaction. Market participants that do not do so risk additional regulatory intervention. This is particularly important in the case of management buyouts, where the conflicts are especially acute and key decisions about access to confidential information and group formation can have material impacts on the outcome of the transaction.

For further detail, see our Osler Update entitled “New guidance on special committees and going private transactions” on osler.com.

ESW/Optiva decision

Since May 2016, bids under National Instrument 62-104 Take-Over Bids and Issuer Bids have been subject to a mandatory minimum tender requirement of more than 50% of the outstanding securities of the class that are subject to the bid, excluding those beneficially owned by the bidder and its joint actors. In the first decision addressing a request for a discretionary exemption from this 50% mandatory minimum tender requirement, the OSC dismissed the application for exemptive relief brought by ESW Capital Inc. (ESW), the largest shareholder of Optiva Inc. (Optiva).

ESW sought an exemption from the mandatory minimum tender condition before it would make an unsolicited offer to acquire the outstanding shares of Optiva not already owned by ESW. It did so because of its concern that blocking positions held by other shareholders would prevent its proposed offer from succeeding. Rival shareholders Maple Rock Capital Partners Inc. and EdgePoint Investment Group Inc. were expected to reject ESW’s offer to acquire all of the Optiva shares it did not own. The pair collectively owned approximately 40% of Optiva, which, when combined with ESW’s 28% stake, was sufficient to block ESW’s bid from meeting the 50% mandatory minimum tender condition, unless a discretionary exemption was granted.

Although the availability of exemptive relief under NI 62-104 is necessarily a fact-specific enquiry, the OSC order demonstrates, and reinforces previous decisions to the effect, that the Commission is reluctant to interfere with the rules prescribed in the Canadian take-over bid regime absent facts requiring intervention on public interest grounds. The decision follows a 2018 decision where the OSC also declined to deviate from the established rules of the take-over bid regime in the context of the CanniMed/Aurora take-over battle. Reasons for the ESW/Optiva decision have not yet been released.

Yukon Court of Appeal upholds transaction value in dissent decision

In its decision in Carlock v. ExxonMobil Canada Holdings ULC, 2020 YKCA 4, the Court of Appeal of Yukon (Court of Appeal) found that the negotiated deal price was the fair value of the dissenting shareholders’ shares in connection with the 2017 acquisition of InterOil Corporation by ExxonMobil Canada Holdings ULC. The Court of Appeal’s ruling overturned the earlier decision of the Supreme Court of Yukon (Trial Court) which awarded the dissenting shareholders a surprising 43% premium to the negotiated deal price, which was itself a topping “superior proposal” in respect of an agreed-upon transaction.

This judgment signals that Canadian courts will view the negotiated deal price in public M&A transactions as a strong indicator of fair value, consistent with recent decisions on this issue in Delaware and prior decisions in Canada. This decision provides market participants with a clear and detailed formulation of this principle, overturning the surprising ruling of the Trial Court. Further, the decision confirms that corporations are not required to run an auction process in order to obtain fair value for their shares.

For further detail, see our Osler Update entitled “Yukon Court of Appeal upholds transaction value in dissent decision” on osler.com.

Outlook

We are currently observing a strong rebound in Canadian public target M&A activity and the outlook for 2021 is strong. We anticipate that the lessons learned from deal-making during the COVID-19 pandemic will continue to inform market practice going forward.